Renting Out My House Guide | Tax, Letting Agents, Insurance & Laws

- Renting out your house & the finances

- Getting your property ready

- Regulations when renting out your property

- Landlord insurance

- Landlord mortgages

- Tax returns for buy to let property

- What does a letting agent do?

- Breakdown of letting agent charges

- Letting agent fees near you

- How to rent out your house & buy another

- Case study: How I rented out my home

- Renting out your property FAQ

“Should I be renting out my house?” is a question many homeowners ask themselves from time to time.

Renting out your house can be daunting & cause a lot of stress. You need to deal with tenants, regulations and property maintenance. However of course, renting out your house is a great way to generate income.

Like many landlords, you may be opting to get a letting agent when renting out your property. Getting someone run your property will help alleviate a lot of the problems & stress being a landlord creates.

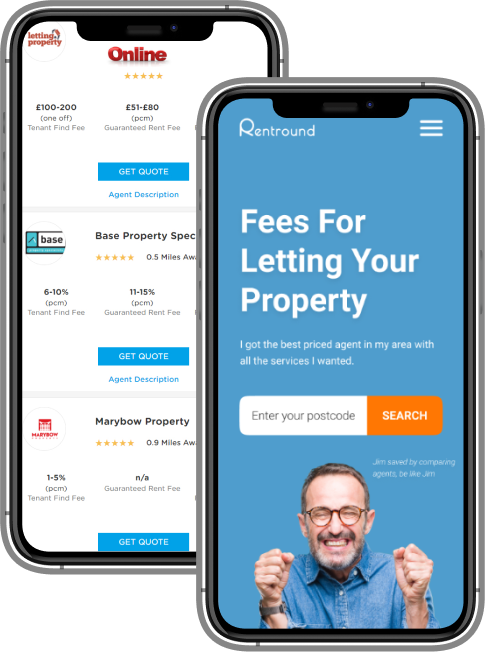

When renting out your house and getting a letting agent to help, you need to be aware of the types of services on offer and the fees they will incur.

Below are the services & fees letting agents offer to make your life easier. In addition, tips to ensure you pay suitable letting agent fees so you don’t get ripped off.

A letting agent manager can take on a subset of activities or you could select full management of your property. This is where you are completely hands off.

The type of service you choose will impact the letting agent fees that are charged. Rentround helps you save on letting agent fees when renting out your house. You just need to enter your postcode then we scan the market and compare the services & fees of reliable & reputable agents in your area. It’s completely free to use.

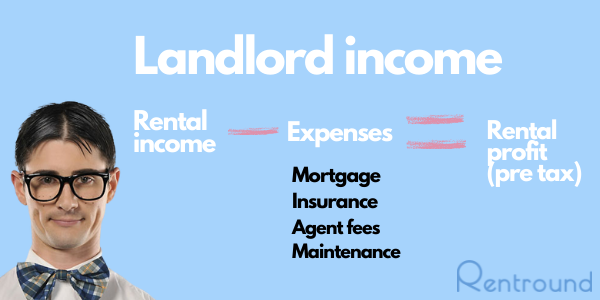

1. WORKING OUT THE FINANCES

You need to first consider the cost of renting out your house and how your finances will be impacted.

The costs you need to consider are:

- Additional mortgage costs

- Your expected rental income

- Your landlord costs

ADDITIONAL MORTGAGE COSTS

Your current mortgage may be a residential mortgage, which means the mortgage is suitable for a property you are living in yourself. When you decide to rent your property out, you will need to talk to your lender about switching the mortgage to a buy to let mortgage.

A buy to let mortgage is suitable for properties that are being let out to tenants. These types of mortgages commonly require a higher interest rate and require a larger deposit.

See our overview of buy to let mortgages to learn more.

YOUR EXPECTED RENTAL INCOME

You need to understand how much rent you’ll get from your property. This is a key figure to work out your profit when renting out your house.

If you’re planning to run your property as a HMO, check out our HMO rental income calculator to see expected rental incomes.

Alternatively you can throw your postcode into Zoopla and see similar properties and their rental charges. To get a more accurate rental income forecast, talk to a letting agent, who will assess your property individually.

YOUR LANDLORD COSTS

You will incur various costs as a landlord that need to be factored into your profit calculations.

These include insurances, renovation work (to make sure the property is safe & secure), safety certificates and the costs of finding tenants & managing the property. Unless your an experienced landlord, you may wish to seek the help of a letting agent.

A letting agent will obviously have a cost, however will take on a lot of the activities on your behalf. We go into more detail about how a letting agent can help you rent out your house and their costs below.

2. GETTING YOUR PROPERTY READY TO RENT OUT

Your property must be in a reasonable state before you rent it out. You need to consider safety features such as the property electrics & gas infrastructure. Issues with these types of things can put landlords in big trouble. In addition electric & gas features need to be certified by a qualified professional before you let out your property.

Then there are features that you may wish to renovate to improve your properties rental income potential. Paint work, windows, carpets and doors can go a long way in sprucing up a property to increase rental values. Of course, fixing things in your property does incur a cost.

When renting out your property and trying to figure out the costs of a renovation, you can use Rentround’s renovation cost calculator.

3. REGULATIONS WHEN RENTING OUT YOUR PROPERTY

Every landlord is obligated to perform their job both ethically and legally.

While cutting corners might seem like a good idea at first (and save you time and money), in the long run, it’s never recommended that you break the law.

Not only will it destroy your reputation but you may lose your license. With that being said, here are a few of the regulations, obligations, and laws that every landlord should know and follow.

LANDLORD LICENSING REQUIREMENTS

The Housing Act of 2004 introduced a landlord licensing scheme that all landlords must follow. If you own a property in a selective licensing area, you must obtain a landlord license from your local council before legally letting the property.

Failing to get this license could result in a fine of £30,000. All landlords must qualify for this license, which includes proving that you’re acting within local laws and properly managing all properties.

These guidelines are detailed by your local council.

STARTING A NEW TENANCY

Once you have the proper licensing requirements, you can start a tenancy. But before you let your property and start collecting rent, you need to provide certain information and paperwork to the tenant.

If the tenant you choose has an assured shorthold tenancy (AST), you must legally protect it using a government-backed scheme within 30 days of collecting the deposit. You’re also required to serve the tenant with the following items:

- A gas safety certificate

- An Energy Performance Certificate (EPC)

- A copy of the latest “How to Rent Guide”

Failure to comply could lead to penalties totaling three times as much as the original deposit. It may also interfere with the eviction process if you’re forced to serve tenants with a Section 21 notice (more on this later).

ENDING A TENANCY

Speaking of eviction, there are certain ways to end a tenancy legally. If you choose to end a tenancy early or repossess your property you can do so in two ways — by serving a Section 21 notice or a Section 8 notice.

Section 21 Notice

There are certain steps you must take before the tenancy begins that allow you to legally end it with a Section 21 Notice. This includes providing tenants with:

- A copy of the government’s How to Rent Guide

- A valid EPC (Energy Performance Certificate)

- A valid Gas Safety Record (if applicable)

If you collect a deposit, tenants must also receive:

Detailed information about how the deposit is protected (by one of the three acceptable schemes)

- Deposit protection leaflet

- Certificate proving the deposit has been registered

A Section 21 notice is invalid if the tenant files a legal complaint about the condition of the property.

Section 8 Notice

Section 8 notices can be given in several situations. Some are based on a judge’s order while others are on mandatory grounds. One such incident is when a tenant fails to pay rent for two months or more. If you’re unsure about the grounds surrounding Section 8 notices, check with your local council.

SAFETY REGULATIONS

Another major responsibility of landlords is the safety of both the property and the tenants. Several guidelines and regulations surround these safety standards.

Electrical Safety

Electrical safety is an important part of the letting process. Landlords must guarantee that all electrics are safe and up to code.

This includes any portable appliances on the premises. All electrics need to be in safe, working condition.

A new law requires all landlords to hire a professional electrician to perform a test every five years. You should also keep a record of the inspection as a reference.

Fire Safety

All rental properties must have both carbon monoxide detectors and fire alarms installed before tenants move in.

It’s also recommended that there’s at least one fire extinguisher on the property. If your property is multiple levels, a smoke detector must be installed on every floor.

All rooms that contain a solid fuel-burning device must also be equipped with carbon monoxide detectors. All detectors should be up-to-date and in working order before letting your property.

Gas Safety

If your property has a gas supply, you must have a gas safety inspection done each year. Once complete, you must provide a copy of the Gas Safety Certificate to the tenant. This inspection will ensure that all pipes, air vents, installations, and pipework are in safe, working order.

IMMIGRATION ACT OF 2016

This Act was enacted on 1 December 2016 in England. All UK landlords must perform certain checks to ensure that prospective tenants have the right to legally live in the country before letting property to them.

You must collect and record the tenant’s visa, passport, and other identity information. If you let property to an unqualified tenant (or one that doesn’t have the legal right to let), you will be held liable. This could result in unlimited fines and up to 5 years in prison.

The good news is, if you’ve taken all the necessary steps to legally end the tenancy and evict the tenants in a reasonable amount of time (three months of discovering the tenant cannot legally rent in the UK), you can defend your case and avoid fines and jail time.

GDPR FOR LANDLORDS

GDPR is a set of rules that went into effect on 25 May 2018. While the rules apply to landlords, they were created to give EU citizens more control over their personal information and data.

Under the GDPR guidelines, all landlords are considered data controllers and therefore need to process and handle all tenant information securely.

Landlords must inform tenants of all data they are collecting, why it’s necessary, how it will be used and stored, as well as how long the landlord plans to keep the information on record.

Landlords must enact a privacy policy that clearly states how and why tenant information is collected and exactly how it will be used.

LANDLORD OBLIGATIONS

In addition to landlord guidelines that are enforced by law, there are also obligations that every landlord has. These include repair and health and safety obligations.

Repairs

As the owner of the property, landlords are responsible for all repairs to the exterior and interior of the structure.

Major issues include repairs on the walls, roof, chimney, gutters, and drains. Landlords must also ensure that all equipment for supplying electric, gas (if applicable), and water to the property is in safe working order.

You need to give tenants adequate notice if you need access to the property to inspect the problem and perform repairs.

Some landlords choose to list how much notice will be given in the tenancy agreement.

Maintenance

Landlords are also responsible for the safety and maintenance of the interior of the structure including (but not limited to) all sanitary areas, heating and hot water installations, sinks, baths, and heating and cooling systems.

If the tenant has a fixed tenancy contract for over 7 years, the tenant becomes responsible for these issues and the landlord can’t be held responsible for any damages caused by the tenant.

4. LANDLORD INSURANCE

From car insurance to health insurance, this protection is in place in case you need it. Have you ever considered insurance for renting out your property? Landlord insurance is designed to protect you and your property against unexpected damages. But, is this type of insurance a necessity?

Some landlords neglect to obtain landlord insurance because they don’t want to pay the added expense. Unfortunately, this can be a costly mistake in the end. You should look at it as a long-term investment instead of a short-term expense.

Keep reading to learn more about what landlord insurance is and what your options are when renting out your property.

LANDLORD INSURANCE EXPLAINED

Landlord insurance protects you against accidents, damage, and other financial losses when renting out your property.

Accidents are a part of life. If you don’t have landlord insurance, you’ll be forced to pay out of pocket for damages, accidents, or lost rent. Landlord insurance covers unforeseen events like fire, weather damage, or even theft.

Depending on the type of policy you choose, you may have coverage for both your property and its contents. Loss of rent is another coverage option you can add to your policy.

If you want specific items covered under the landlord insurance policy you choose, here are a few options:

- Intentional damage or theft by tenants

- The cost to replace keys and locks

- Replacing fixtures and fittings

- Accommodations

- Water leaks

- Subsidence

Not getting landlord insurance is a risk. You need to make an informed decision when renting out your property.

Consider things like the value of the home and the items inside it, maintenance costs, the reliability of your renters, and where the property is located.

THE COVID-19 IMPACT ON LANDLORD INSURANCE

There are a few things you need to know about obtaining landlord insurance during the recent Coronavirus pandemic.

Some governments have passed laws that prevent landlords from performing evictions for 90 days.

These laws protect both tenants and landlords using what’s known as a payment holiday. The intent is to ease any financial burdens incurred due to the virus.

IS LANDLORD INSURANCE NECESSARY?

No. Landlord insurance isn’t a must but it’s highly recommended. Most people don’t have enough money in the bank to cover any extreme or serious damage to their rental properties.

You can’t predict things like natural disasters, unreliable tenants, or theft. Landlord insurance is a safety net for your expenses and offers peace of mind when renting out your property.

WHAT KIND OF LANDLORD INSURANCE SHOULD I GET?

Knowing the types of landlord insurance policies available might help you make a more informed decision.

Things to consider are your budget and the value of your property and its contents.

You can start with a basic policy and add-on different line items from there, just know that the more coverage you get, the more expensive it will be.

Building Insurance

Building insurance is the most common and basic type of landlord insurance coverage.

This type of policy will cover the cost of repairing the structure of your property in the event of weather or tenant damage.

Natural disasters include floods, hurricanes, or fires. Tenant damage is generally vandalism or theft.

Content Insurance

In addition to the property itself, many landlords want to protect the contents as well.

Most standard policies cover property contents as well, which include both furniture and appliances.

This is especially important if your rental property comes fully furnished. If the renters are furnishing the space themselves, they need to obtain their own content insurance.

Legal Expenses

Renting out your property comes with certain legal requirements.

Legal expense insurance covers any legal costs associated with going after unpaid rent, performing evictions, or personal injury claims made by tenants.

Accidental Damage

Accidental damage happens and you can’t predict it.

Common household accidents include broken windows, damage to the floors and walls, burns, spills, and the like. Accidental damage coverage helps absorb some of the financial costs associated with these types of repairs.

Landlord Home Emergency

One of the hardest parts about being a landlord is responding to your tenant’s needs 24 hours a day, 7 days a week.

With landlord home emergency coverage, you can provide your tenants with around-the-clock assistance and support without the inconvenience.

This type of insurance policy covers things like a broken water pipe, broken boiler or furnace, or loss of power.

Rent Guarantee

No matter how much research or referencing you do, unreliable tenants slide through the cracks.

When dealing with irresponsible tenants, non-payment is the biggest issue. Rent guarantee coverage helps you get paid on time even if your renters refuse to pay.

After two months of non-payment, landlords can place a claim and collect eight months of back rent. The average rent guarantee policy covers up to £2500 a month in rent.

Liability Insurance

Damage to your property and its contents shouldn’t be your only concern. If your tenants are injured on your property, they can go after you for their medical bills and expenses.

Liability insurance is also known as public liability or landlord liability and helps protect your finances in the event that your tenants are seriously injured.

Many injured parties will turn around and go after you for their medical bills and related expense. Liability insurance will help cover both legal costs and whatever payout the tenant receives.

LANDLORD INSURANCE IS WORTH THE INVESTMENT WHEN RENTING YOUR PROPERTY

When it comes to renting your property, some landlords try to cut corners and expenses whenever possible.

Landlord insurance isn’t one of those expenses! Although insurance coverage isn’t required, it offers both peace of mind and financial security.

Not only does it protect your property and its contents but it also offers financial security in the event of accidental injuries or unreliable tenants who fail to make their payments on time.

Landlord insurance coverage is a small price to pay for the protection you receive.

5. YOUR MORTGAGE WHEN RENTING OUT YOUR PROPERTY

You’re unable to just start renting out your property without switching your mortgage to a buy to let.

Renting out your property results in more risk to the lender, so usually they’ll want you to switch your mortgage (which commonly includes a higher interest rate)

WHAT CRITERIA MUST LANDLORDS MEET TO OBTAIN A MORTGAGE?

- The biggest factor when obtaining residential mortgages is your salary. Buy to let mortgages are different because they’re based on the rental income you expect to receive. Try to establish rental income higher that’s 20-30% higher than your monthly mortgage payments.

- In addition to the rental income, many mortgage lenders require you to prove a minimum annual income of £25k.

- Most lenders expect an LTV rate of between 75-80% on all deposits.

- Most buy to let mortgage lenders won’t allow the maturity of the loan to exceed 75 years.

- Some lenders even look at if you’re planning on getting a letting agent or property manager to help run your rental property – this is especially the case for first time landlords

ARE INTEREST ONLY OR REPAYMENT LOANS BETTER FOR LANDLORDS?

When it comes to selecting a mortgage, landlords must choose between a repayment option or interest only.

Monthly mortgage repayment options carry higher monthly costs, which reduces immediate income but also lowers your property debt. Interest-only mortgages offer lower monthly payments since you’re only paying the interest on the loan, not the debt portion. This results in higher monthly income but, also, higher debt.

Once the mortgage term is over, you need to pay off the debt in full. Many landlords choose to either remortgage or sell the property at this time to cover the cost.

This last option isn’t without risk. If you don’t sell your property for the predicted price, you’re still responsible for paying off the remaining mortgage amount.

The good news is that 40 years of market analysis shows that this is a low-risk option, especially for landlords who’ve had their property for several years.

An interest-only mortgage reduces the on-going cost of monthly mortgage payments until you’re required to pay off the debt in full.

RISKS FOR LANDLORDS TO CONSIDER

No investment is without risk. If you’re buying a property for rental purposes, here are a few risks to look out for.

Rental Income

A landlord’s main source of income for paying their monthly mortgage is rent. Vacancies or the inability to find a reliable tenant could leave you with several months of lost income.

Late payments are another problem for landlords using rental income to repay their mortgage. Too many vacant months can result in late mortgage payments and possible repossession of the property.

One way to handle this risk is by hiring a letting agent or property manager that offers guaranteed rent services. This safeguard guarantees that landlords receive rent even if the tenant defaults.

Property Damage

Although wear and tear are normal, significant property damage can create a major problem for landlords. Not only are you responsible for fixing the damage (although there are some safeguards against this), significant damages could prevent you from renting the property for long periods of time, resulting in loss of income.

Some lenders will offer a payment holiday that freezes your mortgage payments for up to 6 months.

You’ll need to repay these frozen payments once you start receiving income again. In some cases, your landlord insurance will cover the cost of damages. If your insurance is void or the damage doesn’t fall under your current policy, you may struggle to make ends meet.

To protect yourself against this risk, it’s recommended that you create a savings account for such an event.

Dips in the Property Market

Financial crises happen, often without warning. This can reduce your property value and make it nearly impossible to sell.

Depending on how long you’ve owned your property, you may need to wait-out potential property crashes. If you find yourself in a position where you have to sell (like coming to the end of your interest-only mortgage term) or you can’t cover your mortgage payments and are facing repossession, you may need to sell at a lower price than expected.

In some cases, buy to let mortgages are on fixed terms. After this time period ends, the initial interest rate switches to a standard variable rate (or SVR). This rate is often much higher than the original fixed term.

If you want to renew your mortgage during a property market crash, you might find that the property value isn’t enough to cover your mortgage or the loan to value rate has dropped. In this case, you’ll either need to cover the difference yourself or accept a higher rate.

An additional problem is that the economy generally takes a hit during a property market crash as well.

This means an increase in unemployment. Now they’re faced with the loss of income, higher mortgage payments, and lost property value, creating a desperate financial situation. ‘

Increase in Interest Rates

At the time of this writing, mortgage interest rates were at an all-time low 0.01%!

This was good news for landlords seeking affordable lending options.

During the duration of your mortgage if interest rates increase, so will your monthly payments.

Available rates would also be higher, raising costs for any landlords seeking to renew their mortgages.

International Pandemics

The year 2020 will always be synonymous with the world’s first true medical pandemic – Covid-19.

The Coronavirus put the entire world on hold. People were forced to work remotely, leisure activities were virtually non-existent and the property market was frozen.

Landlords and property owners soon discovered that selling a house during a pandemic is very difficult. It’s hard to schedule viewings due to exposure and the risk of contracting the disease. Solicitor teams and letting agents also have limited availability.

If you’re desperate to sell your home during a pandemic, chances are, you won’t get a fair price.

Partnerships

Some property purchases are done under partnerships. The initial cost of the property or shared risk are two reasons more landlords are considering partnership purchases.

Unfortunately, shared risk also means shared ideas and decision making. Two partners may disagree on how to manage the property.

Disagreements involving large sums of money and potential legal proceedings can run up your bill and stress level.

WHERE CAN YOU FIND A BUY-TO-LET MORTGAGE?

There are mortgage lenders everywhere you look. Since you’re making a large financial investment, it’s best you do your research and shop around.

Sites like Moneyfacts offer comparisons of buy-to-let mortgage rates and lenders. Tools like this help you to reduce your biggest monthly expense — mortgage payments.

6. TAX RETURNS FOR BUY TO LETS

Regardless of your profession or line of business, you have to pay taxes on your income. As a landlord, that means paying tax on collected rent.

Here we’ll explore how much you have to pay and how income taxes are applied to rental income.

HOW TO CALCULATE TAX ON RENTAL INCOME

As a landlord, you’re required to pay income tax on any profit associated with your rental properties.

But what is your income? In short, it’s whatever money is left after you subtract associated expenses or allowances from your total rental income. If you own multiple properties, it applies to the total of all expenses and income.

If you have a mortgage on any of your properties, you can add a certain amount of mortgage interest to your expenses.

WHAT IS CONSIDERED RENTAL INCOME?

Before you can do any calculations, you have to figure out exactly what your rental income is. In most cases, collected rent is your primary source of income as a landlord. But rent isn’t the only expense tenants are required to pay.

Depending on your tenancy agreement, other tenant income may include utility bills (including heating, hot water, etc.), cleaning expenses, and repairs in the event you charge a non-refundable deposit.

Any money left over from a returnable deposit at the end of a tenancy is also considered rental income.

Any expenses you incur from letting the property are considered tax deductible. The percentage of your mortgage interest rate can also be applied as deductible, although in some areas, this relief has been eliminated.

WHAT RENTAL INCOME IS TAXABLE?

Let’s look at an example of a rental income situation to help you better understand what income is taxable.

Let’s say a landlord that charges £1,000 per month in rent. Regardless of the monthly bills and expenses, you have to consider this entire amount when considering rental income. Some of these costs will be viewed as expenses later on).

If, at the end of the tenancy agreement, the tenant agreed to apply their £500 deposit to the cost of repairs, this would count toward your rental income.

Even though the rental income total for the year would be £12,000, the landlord would have to include the deposit and declare £12,500 in total.

On the other hand, they’d also be able to deduct the £500 they spent on repairs as an expense.

LANDLORDS WITH MULTIPLE PROPERTIES

If you own and let multiple properties, you can lump all of your rental income and expenses together.

That means that expenses from one property can be deducted from the income earned on another.

There is one situation, though, where rental properties are treated as separate entities. If you own a share in a rental company or business that earns income, this is considered as separate income from your other rental properties.

You can’t use income from a rental property to pay off expenses associated with the rental business. International and overseas rental properties are also treated differently. You can’t lump your UK properties with those in Italy or Spain.

You’ll find a separate section on your tax paperwork for declaring these overseas properties.

HOW MUCH TAX ARE YOU REQUIRED TO PAY ON RENTAL INCOME?

Rental income is taxed as the same rate as any other income you receive from a business or unemployment.

Depending on which tax bracket you fall into, you can expect to pay 0%, 20%, 40%, or 45%. Rental income is added to all other income you receive, which means you may advance to a higher tax bracket.

WHEN ARE RENTAL INCOME TAXES DUE?

The tax year runs from 6 April to 5 April. You’re required by law to report and declare income for the previous year, regardless of when you’re paid. You can deduct any approved expenses connected to completed work for that particular year, regardless of when you pay the bill.

TRADING INCOME VS RENTAL INCOME

Some landlords offer services that exceed what’s considered normal or expected.

Things like meals, laundry, or cleaning all fall under the category of trading income, not rental income.

If you run a hotel, guesthouse, or B&B, all of your income is considered trading income. You can also claim rent-a-room relief when dealing with trading income, as long as you offer a furnished property as part of the agreement.

COMPLETING A RENTAL INCOME TAX RETURN

If you don’t receive a tax return form, you need to notify the HMRC of your rental income no later than 5 October after the end of that tax year, or 5 April.

If you earn regular rental income on a property, you’re also required to fill out a self-assessment tax return.

The deadline for submitting paper tax returns is 31 October. Online returns have a deadline of 31 January of the following year.

These returns are broken down into a few different categories.

MAIN TAX RETURNS

If your total income totals more than £10,000 for the previous tax year, you have to fill out a main return form. If your income is above £2,500 after rental expenses (letting agent fees, property manager fees, property costs, maintenance etc) and deductions, you’re also required to complete this form.

Anyone earning under £2,500 will have their taxes automatically collected from HMRC using the PAYE system, but only if you’ve been taxed this way in the past through your pension, salary, or other system.

If your rental income is from UK holiday lets or other UK properties, you’re required to complete UK property pages.

International properties require Foreign pages. Hotels, guesthouses, and other trades are considered self-employment ventures and you’re therefore required to complete self-employment pages.

This also applies if any portion of your income is considered trading.

DECLARING LOSSES

You can also declare some losses on your UK rental properties. These can be carried forward and used toward future income and profits.

For example, if your rental income for the 2019-2020 year totaled £7,500 but you had claimable expenses that totaled £10,000, you could declare a loss of £2,500.

While you can’t legally offset this against your taxes on other income, you can apply this loss to your tax return for the following year. For example, if in 2020-2021 you profited £8,000, you would apply your £2,500 loss from the previous year to this amount. Now, you’d only owe taxes on £5,500

PAYING TAXES AFTER SELLING A PROPERTY

So, what happens when you decide to sell your rental property? In this situation, you’re required to pay a CGT, or capital gains tax.

Certain rules apply if the rental property also doubles as your main living residence.

Otherwise, selling a rental property is the same as selling any other asset. You’ll pay the basic taxpayer rate of 18% or 28% if you’re an additional-rate taxpayer or higher.

At the date of this writing, all CGT are due by 31 January the year after the property sale occurred. Depending on the date of the sale, you have between 9 and 18 months to pay. As of April 2020, all CGT on properties must be paid within 30 days of the sale.

7.USING A LETTING AGENT WHEN RENTING YOUR HOUSE & WHAT DO THEY DO?

The list of things a letting agent does to help rent out your property varies per agent. Usually, letting agents offer one off services such as finding you a tenant. Or on the other hand more in depth services such as full management of your property, leaving you completely hands off when renting out your house.

Below are some of the common activities that a letting agent will do.

A. FINDING AND SCREENING TENANTS WHEN RENTING OUT YOUR HOUSE

A guide on what a letting agent does to help rent out your property needs to start with their bread and butter. The critical role of a letting agent is finding you tenants. They know the best marketing routes, handle online questions/property viewings and rent valuations

As they manage multiple properties, they also get better cost rates from online advertising agencies. It’s not just finding you tenants. The letting agent needs to answer potential tenant questions, vet their history and handle the initial paper work.

Finding tenants

So how does a letting agent find tenants when you decide to rent out your house?

The most common and effective way is through online portals such as Zoopla & Right Move.

Thousands of potential tenants use these sites to search for rental properties. Once a tenant likes a bunch of properties they like, they’ll contact the letting agent to get more information and/or arrange a viewing.

Either the letting agent, or the property owner will conduct the viewing. Usually if you’re opting for an online letting agent, getting the manager to conduct the viewings will incur an additional fee.

So why can’t private landlords looking to rent out their property just find tenants from Zoopla & Right Move themselves? Unfortunately these portals don’t work with private landlords.

Finding a letting agent – Quick tip

When renting out your house, look at current listings letting agents have featured on the portals already. Keep a look at for those that have good quality pictures and include a good amount of detail of the advertised properties. These letting agent are likely to fill properties quicker and may work best for you in terms of finding tenants.

Tenant referencing

The biggest stress to landlords when renting out their house is bad tenants; those that do not pay rent on time, damage your property and the most worrying of all, those that do not leave.

Every landlord wants tenants that

- Stay long term

- Pay rent on time

- Treat the property as a home

Without experience in the complex tenant screening process, you might end up on the receiving end of the much dreaded “tenant from hell”

Red flags during tenant references differ.

A wide view should be taken when assessing the tenants past behaviour. Examples provided by Blue Crystal include:

1. Bad credit

By far and away, the single predictor of tenants who will pay their rent on time is their credit report and credit score. A bad credit score is a deal breaker in itself. Bad credit score? STOP. Don’t rent to these people! In general, we look for a minimum credit score of 620.

2. Low income.

You don’t have to be a mathematician to understand that if tenants are not making enough in their monthly paycheck, they will not be able to pay the rent. In general, look for a minimum income that is at least 2.5 to 3 times the monthly rent.

3. Criminal history.

A criminal conviction can be a huge red flag.

4. More than 3 convictions in 5 years

If applicants have more than 3 convictions for anything other than traffic violations, it is an indication that they cannot obey rules. Do not look for them to obey your lease.

4. A prior eviction

Such applicants might as well be wearing a sign that says, “I don’t care about ripping you off.” These are people who defaulted on their lease but would not make good on it by moving out voluntarily.

5. Bad landlord references

First of all, if this is your main indicator for determining the eligibility of applicants, you are making a big mistake. Far too many landlords ask tenants to leave, only to give them a great reference. Further, tenants can ask friends to pretend they are a landlord and say great things about them.

Tenancy agreements

Your letting agent post securing a tenant, will draw up a tenancy agreement, between them/you and the tenant.

This document will outline the terms of the agreement, fees, rent, duration of the agreement etc.

A tenancy can be referred back to in the event of any disputes.

Finding a letting agent – Quick tip

Make sure you look closely at your agreement with your letting agent to identify any tenancy renewal fees. Once the tenant’s term completes, your letting agent may charge you a fee to renew the agreement, even if it’s regarding the same tenant.

B. RENT COLLECTION & DEPOSIT SAFEGUARDING

Rent collection & holding deposits is tedious and requires tracking & record keeping. A letting agent can do this on your behalf.

Rent collection

A letting agent will keep on top of rent payments due from tenants. Post collecting the rent, the letting agent will then transfer funds into your account.

This also removes the need for you to have the awkward conversations with tenants when there are late payments, which your property agent will cover off.

Funds are usually collected by card or electronic payments and then sent to your bank account.

Finding a letting agent – Quick tip

Your letting agent fees may be based on the amount of rent received. This will either be based on rent due, or rent collected. If it’s rent due, then you could be left at a disadvantage. If your tenant doesn’t pay the full amount, your letting agent fees will still be the same.

With rent collected, your letting agent fees will be based on what’s actually collected. This safeguards you if a tenant’s rent isn’t paid in full.

Deposit safeguarding

A deposit needs to be taken to cover any damages etc when you rent out your house.

Deposit safeguarding is now required by law. This is to protect all parties involved.

If you’re renting in England and Wales you as a landlord or your letting agent must:

1. Protect your deposit with the scheme within 30 calendar days of receiving the deposit.

2. Send you important information about the deposit protection called the Prescribed Information. This must be done within the same 30 days.

C. PROPERTY INSPECTIONS & CERTIFICATIONS

Property inspections are vital for landlords when renting out their house & required by law. If not done properly, insurances could be void & you could be subject to legal proceedings.

Inspections need to happen before the property is rented out and also take place throughout the tenancy agreement.

Types of inspections include: gas & electrics, plumbing, heating, structural security, damp & leaks and smoke & CO2.

letting agents know the full list of inspections and have the ability to conduct them on your behalf.

D. MAINTENANCE AND REPAIRS

As a landlord renting out your house, you dread being woken up in the middle of the night because your property has a burst pipe, or your weekend ruined because you have to find a plumber to fix a broken boiler.

letting agents cover general maintenance repair work and can be the first port of call for your tenant when emergencies occur.

When damages & faults occur that pose a danger, issues must be fixed immediately. If you don’t & your tenant complains to the council, you may face prosecution and/or fines.

Finding a letting agent – Quick tip

Some letting agent s add a markup on any invoices generated from contractors working on your property. Make sure you cover this with your letting agent beforehand.

If you’re already paying fees to your letting agent for this service, paying markup on top of that can increase costs significantly.

E. LEGAL SERVICES & DISPUTES

The next aspect of services property agents provide to people looking to rent out their property is legal documentation. Most letting agents already have all legal document templates in place to easily adapt to your property. This ensures you are covered from all possible dispute angles & there are no delays in getting your property rented due to legal documentation.

Alternatives of getting your own solicitors to draw up bespoke agreements will take longer & will be far more costly.

letting agents also assist with legal disputes relating to deposits, unpaid rent, property damage etc.

F. FULLY MANAGED WITH GUARANTEED RENT

This service is when a letting agent will manage all tasks related to renting out your house.

You don’t collect rent, screen tenants, draw up rental agreements or maintain the property.

You get the property back in the same condition it was given to the property agent (taking into account wear and tear).

With this type of service however, landlords can expect to pay higher letting fees than the more basic levels of services. Landlords can compare letting agent fees for a variety of services using Rent Rounds letting fee comparison tool

Guaranteed rent

This is a service that ensures you get your rent when you rent out your house, regardless of if the tenant pays or not.

The agent becomes your tenant who sublets the property to others.

8. BREAKDOWN OF LETTING AGENT CHARGES WHEN RENTING OUT YOUR HOUSE

HOW MUCH DO LETTING AGENTS CHARGE FOR TENANT FIND SERVICES?

Letting agent fees depend a lot on how much leg work you’re willing to do when renting out your house. If you want the letting agent to do most of the work for you, opt for a traditional agent. This will cost you between £80 – £200 under a fixed fee upfront term. Commonly traditional letting agents charge 75%-100% up to the first months rent, however there are no upfront costs to cover. Letting agent fees for finding tenants may also cover conducting references, and arranging the tenancy agreement.

HOW MUCH DO LETTING AGENTS CHARGE FOR FULLY MANAGED SERVICES?

When renting out your house and hiring a letting agent, expect to pay 12-18% of the monthly rent.

HOW MUCH DO LETTING AGENTS CHARGE FOR GUARANTEED RENT?

Rental agency fees can run anywhere from £80 to £200 per year. More expensive policies usually have fewer restrictions and lower pay-out periods.

ADDITIONAL LETTING AGENT FEES WHEN RENTING OUT YOUR HOUSE

ADDITIONAL LETTING AGENT FEES WHEN RENTING OUT YOUR HOUSE

With so many letting agents and property managers services on the market, landlords face a host of different additional fees. Sometimes, these fees are already included in the service agreement. If they’re not, the letting agent will charge these fees separately.

As a landlord renting out your house, these are the fees to look out for and required services.

TENANT RENEWAL FEE

One of the main services already included with letting agent and property manager fees is finding you a reliable tenant. Once the tenant is secured, the duration of the rental agreement will be listed in the tenancy agreement.

Once the term ends, you and the tenant may want to continue your arrangement. If so, you’ll need to pay a tenancy renewal fee. While this can be frustrating for many landlords, the agent already did the hard part, which is finding a quality tenant.

Renewal fees cover the cost of writing up a new agreement which includes updating the dates listed and related terms. Don’t try to pass this fee onto your tenants — 2019 legislation has deemed this illegal.

If you don’t want to pay this fee and are willing to do the work yourself, make sure it’s not included in the written agreement you have with your letting agent or property manager.

Another option is to switch the tenant to “periodic” once the term in the original agreement expires. This means that the tenancy is now a “rolling” contract with no defined end date. Rolling contracts usually follow the original terms and conditions.

How much are letting agent tenancy renewal fees?

Curious as to how much these fees will run you? Most agents charge between £45 – £120 to renew a tenancy agreement when renting out your house. The good news is, not all agents will charge for this service so be sure to check the fine print and check for specific rental agency fees.

HOW DO RESERVE FUND FEES WORK?

In life, and in rental agreements, accidents and damages can happen. To protect themselves, property managers and letting agents create a stash of money to cover any damages to the property — this money is known as a reserve fund.

Just like landlords don’t want to chase renters for payment, your agents don’t want to foot the bill for possible damages and then charge landlords. Reserve fund fees guarantee that the money they need for repairs is available right away.

If the agent taps into the reserve fund, the money is usually returned after the agreement with the landlord is over.

How much are letting agent reserve fund fees?

So how much are agent reserve fund fees when renting out your house? It all depends on the property value. The larger the property and the more valuable, the higher the risk of damage (and more expensive). Fees can range from £200 – £1000.

NECESSITY BILL FEES

One of the luxuries of hiring a letting agent or property manager when renting out your house is not having to worry about the daily responsibilities of owning a rental property. If this describes you, paying bill fees might be well worth it.

Obviously, you need to pay for the basic necessities of owning a rental property. This includes the mortgage, gas, electricity, and other service fees. This also means the hassle of managing the bills. Landlords can eliminate the headaches by passing it onto their agents. Now, you don’t need to track which bills are paid, due, or past due.

If you want a letting agent to handle your bill fees, you can expect to pay about 1.5% – 4% of the amount billed.

ADMINISTRATION FEES

Administration fees are some of the most annoying for landlords when renting out their house. They cover tedious things like adding your profile on a system, uploading your bank account details to your agent’s platform, setting up direct debits, and recording your contact information. But for many landlords, paying these rental agency fees are well worth it.

Other landlords speak out against these fees and try to negotiate them at a lower rate or get them completely eliminated. Chances are, the letting agent will want your business enough to wave the fee and continue working with you.

How much are letting agent admin fees?

Different agents charge different admin fees and they can range anywhere between £50 – £200.

EVICTION FEES

Just like accidents happen, sometimes, you get stuck with an unreliable tenant that you’re forced to evict. A few issues can result in eviction including excessive damage or misuse of the property, not paying the rent on time, or falsifying information on the application. When these things happen, you’ll need to start the eviction process. Letting agent and property manager fees can help cover this.

The process includes notifying the tenant and in some cases, taking them to court for payment. Once the situation is settled, you may need to remove the tenant from the residence. Some tenants are more reluctant to leave than others. Agents have the expertise and knowledge about current legislation and laws regarding the eviction process. But they may charge you for their help.

Compare the cost of getting their help and the hassle of handling it on your own. If the agent can handle the eviction process faster and more effectively, it might be worth it. This is also true because the faster the former tenant is out, the sooner you can get a responsible, paying tenant in place. Remember, your mortgage lender won’t wave your monthly fees just because you’re in the process of evicting your tenant.

How much are letting agent tenant eviction fees?

Before you can decide if these fees are worth it, you need to determine what they are. Different services carry different price tags. Serving an eviction notice will run you £120. Hiring a County court bailiff could cost £250 and getting a court order might be as much as £850.

LATE PAYMENT FEES

Just like you expect your tenant to pay on time, agents expect to be paid for the work they do. If your letting agent and property manager fees include maintenance and repairs on your behalf, you may receive a bill for these fees.

The invoice your agent provides should be paid within 14 days. Delaying this payment could result in late payment fees. In some cases, the agent will tap into the reserve fund mentioned earlier.

How much are letting agent late payment fees?

Expect to pay a fixed fee of £30-100 to cover these expenses or 3 -10% of the due payment.

MAINTENANCE FEES

If you plan to maintain the property yourself, you may not have to worry about maintenance fees. On the other hand, if the agent is required to perform the maintenance work, they’ll likely charge you for this (in addition to the contractor fees). This is fair since the agent is coordinating the repairs. Not only do they need to find a reliable contractor to perform the work but they also have to pay the fees upfront on your behalf and arrange for the contractor to get access to the rental property.

How much are letting agent charges for ad-hoc maintenance?

How much can you expect to pay for these service and maintenance fees? Generally, agents charge between 10 and 15% of the total bill to compensate them for their time. Then again, if you’ve already arranged for a fully managed service (including maintenance), you shouldn’t have to pay any additional letting agent or property manager fees.

ESTATE AGENT FEES

Are you trying to sell a property that you inherited or no longer want or need? In this case, your agent will help sell the property and take a commission. The commission covers advertising the property, negotiating part and parcel services, and scheduling showings.

Online estate agents are making an appearance in the property market, giving landlords more options for selling unwanted property. Instead of a commission based on a percentage of the sale value, some online agents charge a fixed fee. This fee stays the same regardless of how much the property sells for. Be prepared though because the lower the fees, the more work falls on you.

Some landlords have the time (and patience) to do this themselves. Busier landlords can’t be bothered and would rather pay the letting agent and property manager fees for peace of mind and a quick sale. Another fee to consider is the one an agent might charge if you sell your property while still under a fixed agreement. This means that even if you sell your property using a different estate agent, you’ve now broken the terms with your current rental agent and may need to pay a penalty or exit fee (more on this later).

How much are estate agent fees?

When discussing a commission, most estate agents collect 1.5 – 3% of the property’s value when sold. When working with an online agent, the fees range from £99 to £1000.

EARLY EXIT FEES

Early termination fees are common in most agreements. And a rental agent agreement is no different. If you’ve signed an agreement with a letting agent or property manager when renting out your house, there’s likely a term associated with it. That means that canceling the agreement before the term is over could result in an early exit fee. This fee is in place to protect the agent against unreliable landlords. Similar to a security deposit paid by the renter to cover damages to the property or late rent, early exit fees protect the agent’s business.

If you break your agreement due to poor service, you can challenge the exit fees. In other cases, if the terms aren’t outlined specifically in the agreement, you may also get away with exiting without any fees. Some things that classify as poor service are failing to collect rent, not properly maintaining the property, or ignoring specific landlord requests. To avoid complications, make sure all stipulations are included in the agreement with your agent. List all exit fees and service costs.

In the event that the agent insists on charging early exit fees, you can follow these complaint procedures

REDRESS SCHEME

One benefit of dealing with letting agents is that as of 1 October 2014, it’s a legal requirement that agents be part of an approved redress scheme. These schemes can help resolve disputes between you and the agent.

Redress schemes protect both landlords and agents, mediating disputes between agents and landlords as well as between agents and tenants when agents fail to deliver services as promised.

Landlords who aren’t happy with the letting agent’s internal complaints procedure or response can take your complaint to one of these schemes. Letting agents must clearly outline which schemes they’re part of. The most popular government-backed schemes are

- The Property Ombudsman (TPO)

- The Property Redress Scheme”

How much are letting agent early exit fees?

So, how much will you be charged if you exit an agreement too soon? Exit fees can run as high as 10% of the remaining rent. You’re also required to pay them for the remainder of the term. This means if you want to end your agreement with six months left (and there are no possible disputes present), and the rent is £1,000 per month, your exit fee would be £100 per month, totaling £600.

TENANT LATE PAYMENT FEES

Another part of the tenancy agreement when renting out your house is how much tenants must pay if they’re late on rent. These late payment fees are in place to encourage renters to pay on time. Letting agents can use a portion of these late payment fees as their commission. Because late payments must be tracked and chased, it’s only right at the agent receives payment. Landlords should negotiate this fee with the agent and include it in the agreement. You don’t want to incentivize the idea that agents can make money off of tenants who don’t pay on time.

How much are letting agent late payment fees?

Plan to pay the letting agent between 5 and 10% of whatever late fees you charge the tenant. Tenants usually pay 5% of the rent as a penalty for not paying on time.

INVENTORY FEES

Landlords must record a detailed list of items contained in the rental property to protect themselves against any damages. This list is essential for dispute resolution when renting out your house. Letting agents and property managers can help you compile these lists for a fee. It may be worth it since performing inventory also includes documenting any missing or damaged items for proof and reference later on.

How much are letting agent property inventory fees?

Having a letting agent or property manager handle inventory could cost you up to £100. Larger homes or properties that include three or more bedrooms might cost double (£200). You can find our letting agent fee calculator at the top of the page.

9. RENTING OUT YOUR HOUSE: THE FEES

All in all there are a range of benefits of getting a letting agent when renting out your house.

You can get a subset of services, or hand over full management of your property.

Now comes probably the most important part of selecting your property or letting agent.. fees!

Rentround enables you to simply enter your postcode and the services you want.

We then provide you the best property agents in your area, based on rating, letting fees and types of properties they manage.

Our service is completely free and we never charge landlords.

Use our comparison tool to start the process of saving on rental costs!

10. HOW TO RENT OUT YOUR HOUSE AND BUY ANOTHER

A common way people increase their property portfolio is by renting out their house & buying another. This is done by using the rental income to cover your existing mortgage repayments. Then either using your savings or by releasing equity in your previous property as a deposit on the next property.

For example, lets say you property is worth £500,000 and you’ve paid off (via monthly payments and your initial deposit) £300,000. This means you have 60% of the properties value as equity. You may decide to negotiate with your lender to reduce that amount. For instance you could add on £100,000 back onto your mortgage, leaving you with £200,000 of the property equity, and £100,000 cash in your bank account. The cash you receive can then go towards purchasing another property.

As discussed above, you may need to switch your current mortgage to a buy to let mortgage. If you’re planning to release some of your equity to purchase the next property, then it’s suitable to do this in parallel as you convert the mortgage to a buy to let.

As you take equity out of your property to purchase the next, your monthly payments on your rental property will go up as you’re borrowing more from your lender. Ideally, you’d like your rental income to cover this additional cost as well.

11. How I rented out my house – A landlords view

The following is the point of view of Nirmal Singh, a recent newbie landlord who has been kind enough to share his experience of renting out his property.

Moving is an extremely stressful event. Not just the moving process itself, but deciding when the time is right.

After closely watching the property market and researching some of the best places to live, I decided to take the plunge. I was in a good financial position since my mortgage was almost paid off but quickly realized that I wouldn’t get the price I wanted for my house. So, I started exploring other options.

One option was renting out my property. I’ve known a few people who have bought and flipped houses for passive income. I mean, look at how popular Airbnbs are and those aren’t usually full-time rentals! I figured with the right tenants and a little TLC to fix some minor issues, that renting out my house would be a lucrative decision. If I planned things properly, I could find and move into my new dream home without the hassle of selling my old property. Instead, I could use it to make some money!

Since I’d never been a landlord before, I wasn’t really sure how complicated renting out my home would be.

Being a landlord, accidental or not, comes with a lot of responsibility. I knew I couldn’t just hand over the keys and walk away without providing the renters some security, assistance, and peace of mind. But I had no idea where to start! What were my legal obligations? Did I need to collect a deposit? Who was responsible for maintenance and repairs? I needed all of these answers before I could take the next steps and start referencing tenants. I also needed to make sure my property was move-in ready.

I started by looking at my house through the eyes of potential tenants. Not only did I need to make sure it was an attractive rental property, but that it was safe. If nothing else, I knew that if a tenant was injured due to my negligence that I’d have to pay. Before renting out my home, I gave it a facelift. I gave the living room, kitchen, and master bedroom a fresh coat of paint and repaired a few holes. I also replaced the kitchen cupboards and added more modern accessories like light and plumbing fixtures.

I removed any personal photographs or items to help prospective renters imagine themselves in the home. I knew from house hunting in the past how important curb appeal was so I also did some outdoor cleanup as well. I’d neglected my garden for several seasons so I did some major weeding and planted some attractive shrubs. I also installed walkway lighting for ambiance and safety reasons.

Once I was happy with how my house looked, I started researching tenants.

It didn’t take me long to figure out that finding reliable tenants and performing background checks would be a long, tedious process that I probably wasn’t equipped to handle.

I also knew that I had a legal obligation to provide certain securities, paperwork, and certifications but wasn’t sure exactly what those were. That’s when I decided that hiring a letting agent might be a good idea.

Although it would cut slightly into my income, it would be well-worth it in the end. Letting agents can handle all the paperwork and legal obligations for the property, along with maintenance and repairs. I work a full-time job and wanted to move almost 30 miles from my rental home, so having a responsible letting agent on hand to answer emergency calls and perform maintenance and repairs was a must! Not to mention, I didn’t want to deal directly with renters if they turned out to be a problem or needed to be evicted. I wanted someone else to deal with the hassle of collecting rent and addressing nonpayment.

After sitting and crunching numbers, I realized that I could rent out my property, use a letting agent, and still make passive income. The best part is, with a reliable letting agent in place, I was able to broaden the search area for my new home. I didn’t have to worry about living close -by in case the tenants needed me for repairs or I needed to perform an inspection.

Once I found an affordable and experienced letting agent, they started referencing tenants right away. They even handled all of the property showings. Once my agent found a reliable tenant to rent out my property to, they also handled the TDS deposit.

I had no idea that I had to enroll in a government-approved Tenancy Deposit Scheme (TDS).

My agent was knowledgeable about all the necessary steps and made sure that I remained compliant with my rental agreement. The agent also provided the renters with all necessary certificates including ones for energy performance, electrical, gas, and other safety requirements. Without these, I could’ve gotten myself in serious legal trouble.

Even though I didn’t plan on becoming a landlord, I’m so happy I did! Now, I can move out of the city without worry and with some extra cash in my pocket.

12. RENTING OUT YOUR PROPERTY FAQ

When renting out your house, follow the below steps. 1. Ensure your property has a rental demand. 2. Talk to your lender about switching your mortgage to cover a rental property. 3. Ensure your property meets the right safety criteria. 4. Get landlord insurance 5.Hire a letting agent to find you tenants & manage your property (if you haven't got the time to manage the property yourself. 6. If managing the property yourself, collect rent, deal with repairs, stay on top of new regulations and manage tenant issues.

For landlords, it's a good idea to get covered with adequate landlord insurance. Insurance can cover you against accident damage, property problems & the right policy can cover you against unpaid rent. In addition, some lenders require landlords to have insurance in place before issuing a mortgage deal.

Before renting out your house, you need to check with your lender that your current mortgage is adequate for a rental property. Then you need to ensure your property is safe and meets regulatory guidelines. If you are looking to sublet your property, you need to check your agreement with your landlord first. In addition, if you plan to run your property as a House in Multiple Occupancy, you may need to apply for a license.

You need to tell your lender that you plan to operate the property as a rental. Usually the lender will charge a fee or increase the % charges on your repayments. Not telling your lender beforehand can result in financial penalties and other types of repercussions, including demanding to pay back all of your mortgage.

For finding a tenant based on a fixed price term, an agent will charge between £100-£600, with the cheaper end of the scale offered by online letting agents. For full management of your property, charges are usually between 10-18% of your monthly rental income.

Your rental income will depend on your property and it's location. The most accurate way to see how much you can rent your house out for is by talking to a letting agent. They will have the local knowledge to understand what you can expect. Alternatively, you can run a search on Zoopla to see what other similar properties are renting out for.

How do I rent out my house?

Do I need landlord insurance?

Can I rent out my house?

Can I rent out my property with a residential mortgage?

How much are letting & property manager fees to rent out my property

How much can I rent my house out for?

Compare Estate & Letting Agents

Find the best agent for your property. Compare fees, ratings & services for free!